Dassana Wijesekera: A Future for Financial Services – The Banking Experience Canvas

By Dassana Wijesekera, Head of Solution Architecture – Open Banking and Financial Services, WSO2

What might the future of banking look like? The consensus today is that this question must be answered starting with a laser focus on the consumer’s need, and rightly so. There is no doubt that today’s consumers are increasingly digital, making use of products and services on multiple channels and devices, sourcing instant, personal and seamless ways to meet their needs. Those less keen have now been pushed over the digital edge by COVID-19 and have most likely bought into these experiences for the long term. However, this places more pressure on traditional businesses to respond with matching experiences or risk becoming irrelevant.

In order to provide a tangible example of what is already possible with existing technology and based on my experience in working with banks to enable their journeys in the API economy, I have devised the “Banking Experience Canvas” —a product concept that illustrates what banking experiences could look like.

From branch to mobile to platform

As with any industry, financial services has (albeit slowly) responded to the digital revolution. First, we saw existing products and services being made available on digital channels. Now, banks have bought into “doing digital” more completely, seeing the benefits of collaboration with service providers from both the financial services domain itself and from related verticals, to help deliver more relevant consumer experiences.

We can already see this playing out at scale, as a result of increased regulation and market-driven forces such as open banking, with banks collaborating proactively with fintechs to respond more quickly and effectively to changing consumer behaviours. Consumers, both individual and corporate, are already deriving value. For example, “time to cash” on loan applications have been slashed from months to minutes, millions more have been able to prove creditworthiness based on utility and rent payments, and providers are actively exploring ways to deliver effective personal finance management services designed to give us new actionable insight into our spending and investment patterns.

Where are banks falling short?

Even with progress, financial services experiences are still disjointed and in the main driven by the provider, rather than the consumer. The financial steps towards fulfilling personal needs—buying a house or saving for that dream summer vacation—are designed not by the individual, but the service provider.

Take, for example, the process of buying a house. The journey involves several unique steps including figuring out how much we can afford, putting the funding together, analysing properties, negotiating on price, contracting and committing funds. As individuals we will naturally order these steps based on our own unique requirements. While some of us might first identify our dream house and work their way back to what they can afford, others will first figure out their funding plan. This journey is not necessarily linear, and generally involves a fair amount of back and forth between steps, reevaluating decisions made previously based on new information and unresolved concerns. However, the process we must follow is often driven by different service providers addressing different steps in the process from finance, to real estate to legal, and the disjointed independent processes of these different providers. Collaboration is attempted, for example, with redirects to banks on online property portals. But these attempts are still clunky, prescriptive, and ultimately a digital rehash of analog processes. In today’s world, especially where “digital natives” are concerned, this is not a natural or comfortable journey for most.

Can banks do more? Of course. Both to create a better and more authentic experience for the consumer, but also, importantly as a business, to derive the most value possible for the bank from the position of trust held by the bank, and the value and capabilities offered by the bank to partners and end-consumers.

Introducing the Banking Experience Canvas

The Banking Experience Canvas, or the Canvas as I will refer to it from here on, is a new digital model built on three principles. In order to provide a fulfilling and natural experience to consumers, in a way that brings in the most value and return for banks, banking services must be:

- Personal

- Complete, and

- Omni-channel

The Canvas is designed to provide a personal and complete experience to fulfill the need of the banking customer. It also looks at bringing in value-added services outside of the traditional banking domain. This enables banks to improve brand loyalty and customer retention, delivering on the promise of platform banking for banks, partners and consumers. It may also be consumed on the bank’s own channels across mobile, web and kiosk, or on channels operated by partners, picking up from the point of the buyer journey that is the next logical step for each individual consumer.

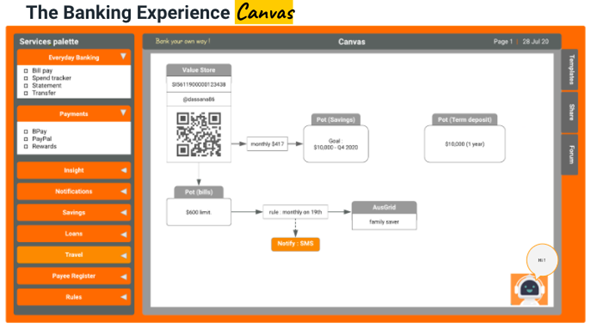

In its essence, the Canvas is designed as a digital canvas where customers will build a workflow arranging multiple individual functions provided by the bank or sourced from partners. These functions range from standard banking functions to value-added services outside of banking. Each banking function can be customised based on individual needs.

Building the Canvas

So how do we make this happen? APIs, microservices, eventing architectures and open banking initiatives across the world provide the necessary technical foundation for this new interaction model.

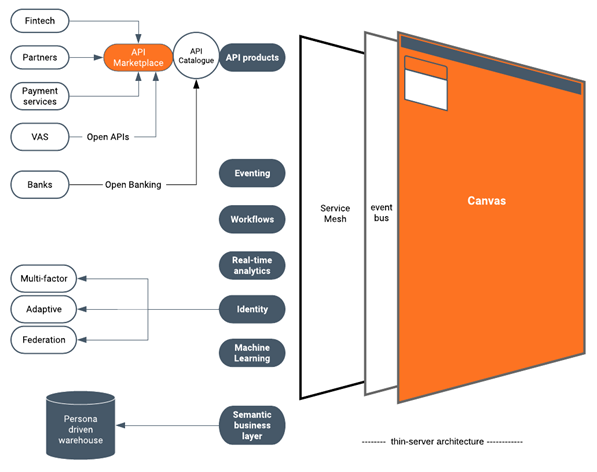

An architectural overview of the Canvas

An important step in the process is to secure access to a strong and complementary set of partners. The bank could look to build a partner ecosystem by providing a collaboration space in the form of an API Marketplace. An effective marketplace setup organises APIs into groups based on their attributes with categories, labels and tags and provides intuitive and self-care workflows to enable fast onboarding. A feature-rich monetisation capability will allow APIs to be monetised in multiple models and is available on any strong API Management platform.

These APIs may be used to build API products which could be added as services on the service palette of the Canvas. The Canvas is presented as an intuitive single-paged application which is paired with an eventing architecture. Each individual banking experience is built as a workflow. Support for eventing architecture, full support for different EI patterns and agility in building these integrations provide the ability for experiences to be built quickly.

The bank also needs to have a strong identity framework that will support many types of identity protocols and identity federation mechanisms. Additionally, to deliver an intuitive and helpful user experience the bank needs to augment real time-analytics capabilities. Providing these integrations, API management, identity and analytics capabilities in a cloud native manner on a single platform makes it easier to build the Canvas.

The conditions for broad collaborative products like the Canvas are now very much in place with concepts like open banking taking hold globally. It’s time for banks to grab the opportunity with the right technology and mindset.

If you would be interested to find out more about WSO2 or your organisation is considering integrating WSO2’s services into your business practices, please visit:

www.WSO2.com/?utm_source=external&utm_medium=media&utm_campaign=wso2ishealthcare_jul20